TOTAL COST OF RISK: The Five Fundamentals of Insurance

HAVE YOU EVER CALCULATED THE UNEXPECTED HIDDEN SOFT COSTS THAT BECOME A PART OF YOUR TRUE INSURANCE EXPENSES?

By Christopher J. Mowery, ARM CRIS Client Service Supervisor

Arthur J. Gallagher & Co.

Everyone knows that premium, losses, and exposures contribute, but the true nitty-gritty of how a company could meaningfully impact their Total Cost of Risk lies in the hidden soft costs a contractor pays out annually in addition to pure insurance premiums. The greatest problem we see from the outside looking in is that many contractors are NOT tracking these costs and how much they impact the bottom-line!

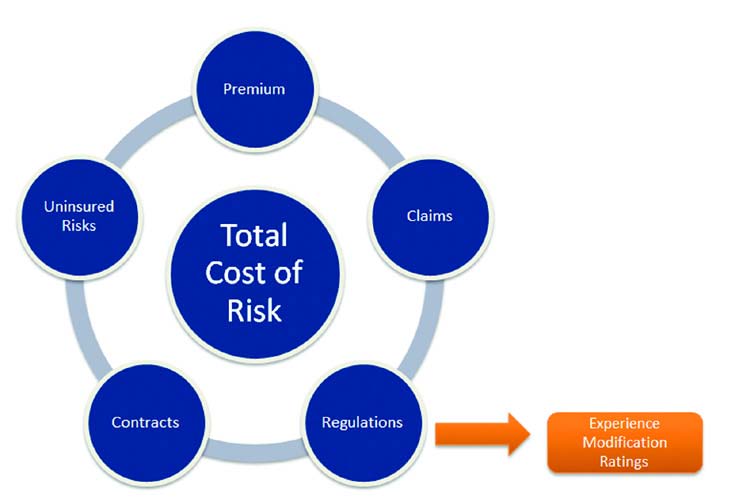

Total Cost of Risk, TCOR for short, is a combination of:

- Hard costs or the actual costs associated with premium and losses within a deductible layer (if any)

- Soft costs or the actual costs associated with return to work programs, safety control, internal management costs, experience modification ratings, medical, replacement workers, etc. Most of the soft costs are under the radar and never mentioned to a contractor.

As much as 50% to 55% of a company’s total cost of risk is in the area of soft costs. These additional costs are in addition to the premium (hard costs) a company is already paying for insurance. We are working on a series of articles that are designed to make you aware of the types of hidden costs that exist as well as provide ideas on ways to eliminate or lessen these costs. A company’s total cost of risk is managed by Five Basic Fundamental Areas: Premiums, Claims, Regulations, Contracts and Uninsured Risks.

This article focuses on a subset of Regulations, specifically a company’s Experience Modification Rating (EMR). Companies are being squeezed on every project to run on very thin margins leaving zero room for mistakes and expenses which are unaccounted for. Any blip in your loss history or exposures can cause a swing with your EMR. Profits earned on jobs today could be diminished in years to come because of the soft costs associated with a company’s EMR from prior years. There is no doubt this impacts a company’s operations financially in a significant way.

Not only does an EMR indicate how safe a company is, it also contributes to the premium a company is paying for Workers’ Compensation coverage. How many jobs would it take your company to replace lost profits from a high EMR? Or how much more successful could your company be if you could bid work more competitively due to lower insurance overhead? Looking at the exhibit below and assuming a company has a 10% profit margin; it would take an extra $300,000 in jobs to pay for a 1.30 EMR. How many free jobs is your company doing a year to pay for your EMR?

Premium EMR Modified Premium

$100,000 X 0.70 = $70,000

$100,000 X 1.00 = $100,000

$100,000 X 1.30 = $130,000

SO WHAT IS NEW IN MANAGING AN EMR? THE ANSWER IS EMR MODELING AND AUDITS.

EMR modeling is a valuable tool for every contractor. Every company has their own individual EMR minimum. In today’s world of benchmarking and analytics we have the ability to evaluate each claim and tell the company how that one specific claim impacts their EMR. EMR modeling provides an analysis that is used to determine how frequency and severity impact the numbers and could also be used to calculate future EMR’s. This modeling can be a very effective tool with field staff when setting reduction goals to ensure they are reasonable and achievable.

Modeling provides us with an inside look at the calculation to see the major contributing factor driving a company’s EMR. We have noticed that frequency claims, the NCCI defines this as any claim less than $15,500 in total incurred (Paid + Reserves), can have a big impact on the numbers. Having a high frequency of small claims impacts the EMR more than one large claim. The reasoning is simple, the higher the frequency of smaller claims the more likely a severe claim will occur. EMR’s are also greatly impacted by lost time claims; monitor your lost time claims verses medical only – medical only claims have a significantly lower impact on the EMR (discounted 70%).

EMR audits further allow us to verify the factors that contribute to the calculation. Have a professional review the EMR for accuracy: verifying payroll, loss totals, and types of injuries. Also, conduct an audit on your EMR 2 to 3 months ahead of state filings (typically 6 months ahead of a company’s EMR effective date) to make sure reserves are set correctly, verify claims, and make sure as many as possible are closed can assure you have a correct calculation.

SO WHAT STEPS SHOULD YOU TAKE TO LOWER YOUR EMR?

- Track your additional annual costs passed on by your EMR.

- EMR Modeling – Determine your company’s lowest possible EMR. Set goals based on the workable EMR, which is the difference between current EMR and lowest possible EMR.

- EMR reduction must be a priority – senior management must be visible in the safety effort and must support improvement.

- Frequently communicate with employees, both formally and informally, regarding the importance of safety.

- Create a Safety Committee – Set safety goals for those with supervisory responsibility. Success in achieving safety goals should be used as one measure during performance appraisals.

- Negotiate PPO savings on medical care.

- Evaluate accident history and near-misses on a monthly basis. Identify trends in experience and take corrective action on the worst problems first.

- Investigate accidents immediately and thoroughly, take corrective action to eliminate hazards and be aware of fraud.

A vibrant and vigilant safety culture is a must. Management teams who approve and direct work activities can exert considerable influence over the operations they run, shaping the way things are done, how managers interpret safety and health policies and promote a safety and health culture among the workforce. Supporting a safety culture with evidence that it will help save money is the best way to convince upper management to get on board. Injured employees drive up company costs in the form of lost work days and compensation costs. By taking a proactive approach to safety, a company can avoid the nuisance of smaller claims and help to decrease or maintain an EMR.

Managing your claims is a must. It is imperative that when an injury occurs it is reported quickly and accurately. Employers need to be proactive on this as it has a direct impact on the overall cost of the claim.

In this day and age, a light-duty, return to work program is not just an option anymore, it is a requirement. It has been proven that light-duty programs cut the number of lost work days in half and workers who are offered light duty return to work twice as often as those who are not. It has also been proven that employees who are off work because of injury for more than 16 weeks seldom return to the workforce and subsequently companies get stuck paying hundreds of thousands of dollars each year in unnecessary costs.

From being competitive and winning new contracts, to paying for a higher EMR than a company should, the above actions should be carefully considered and where possible implemented. It is important to know that a claim stays on a company’s EMR for a period of three years. That is three years of potentially paying a higher EMR when it possibly could have been prevented. Stop doing work for free just to pay for your high EMR. Make the commitment to invest in a healthy and safe work environment today and it will pay for itself tomorrow.

Stay tuned for next month’s installment, the second fundamental of insurance: Contracts.

ABOUT THE AUTHOR

Christopher Mowery is a Client Service Supervisor for Arthur J. Gallagher & Company. He has over ten years of experience marketing and servicing Construction and Risk Management accounts. For more information about this article, Christopher can be reached at Christopher_Mowery@ajg.com. More information on Gallagher can be found at their website www.ajgrms.com.