An Unbalanced Market: Demand, Development and What’s Ahead

By Chris Hancock, CEO, Builders Association of Greater Indianapolis

The U.S. homebuilding industry is operating in an increasingly unbalanced market, shaped by persistent economic pressures, structural supply constraints and evolving buyer behavior. According to the National Association of Home Builders (NAHB), builders across the country continue to face a convergence of challenges that complicate both planning and production. Elevated interest rates remain the most significant headwind, directly impacting affordability and sidelining many prospective buyers. At the same time, inflationary pressures, rising labor and material costs and a chronic shortage of developed lots continue to strain margins. Layered on top of these realities are cautious consumer sentiment, uncertainty in federal policy, and media narratives that reinforce a wait-and-see approach among buyers. Together, these forces have created a difficult operating environment for builders nationwide.

A National Market Under Pressure

Across the U.S., the new home construction market is grappling with the same macroeconomic forces—affordability challenges, higher borrowing costs, labor shortages and supply chain disruptions—but their effects vary by region. While some local markets have demonstrated resilience, national housing production remains below the level needed to meet long-term demand. According to the United States Census Bureau, total housing starts and permits have yet to return to pre–Great Recession norms on a per-capita basis, even as population growth and household formation continue.

This imbalance has resulted in a persistent housing shortage. Freddie Mac estimates that the U.S. is short several million housing units, a gap that continues to widen as new supply struggles to keep pace with demand. The trajectory of the national housing market remains cautiously optimistic, but its stability will depend on how effectively builders, policymakers and financial institutions address three interconnected factors: demand, supply and affordability.

The Demand Is Still There

Despite elevated mortgage rates and inflationary pressures, underlying demand for housing in the United States remains strong. Demographic fundamentals continue to support long-term housing needs. Millennials—the largest generation in the workforce—are now in their prime homebuying years, while Generation Z is beginning to enter the market. According to the Joint Center for Housing Studies of Harvard University, household formation remains constrained not by lack of desire to own, but by affordability and limited inventory.

First-time buyers continue to seek homes that offer more space, stability, and long-term value, particularly as rental costs remain elevated in many metropolitan areas. At the same time, move-down buyers are playing a growing role in the market. Many homeowners are looking to reduce square footage without sacrificing quality, driving demand for well-designed, low-maintenance homes in established communities.

Another important national trend is the aging of the Baby Boomer generation. Longer life expectancy and a preference to age in place—often in homes that were custom-built or significantly upgraded—has reduced the turnover of existing housing stock. Homes that might have traditionally re-entered the market are remaining occupied, further constraining resale inventory and increasing pressure on new construction to meet demand.

National building permit data illustrate this divide. Following the mid-2000s housing crash, new housing authorizations declined sharply and never fully rebounded to prior peaks. While permits have trended upward in recent years, growth has not matched population increases or household formation rates. The result is a structural supply deficit that continues to push prices higher and limit options for buyers.

Home Construction Has Not Recovered from the Great Recession

More than a decade after the Great Recession, U.S. housing production remains structurally constrained. The cumulative underbuilding that followed the housing crash has left the country with a significant backlog of unmet demand. Economists at Freddie Mac and the Urban Institute have consistently pointed to underproduction as a primary driver of today’s affordability crisis, noting that even sustained increases in construction would take years to close the gap.

The Supply-Side Struggle

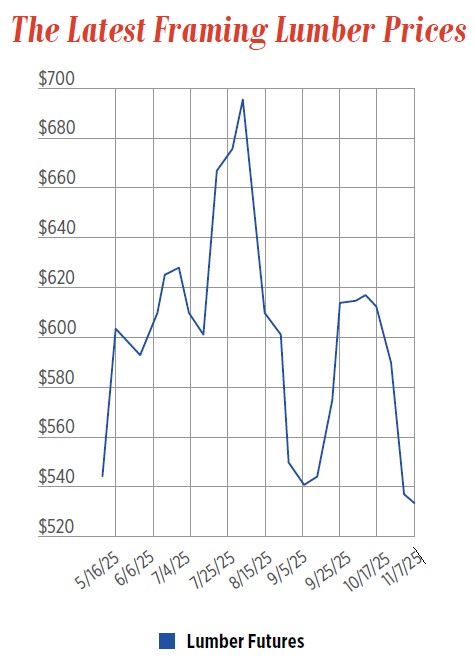

On the supply side, builders face mounting challenges that extend well beyond the cost of construction itself. Material availability, while improved from pandemic-era disruptions, remains inconsistent. Lead times for key inputs such as lumber, steel, windows and mechanical components are still significantly longer than pre-pandemic norms, increasing carrying costs and complicating project scheduling.

Land development has become one of the most significant barriers to expanding housing supply nationwide. The cost of a finished home often captures public attention, but much of the financial burden is incurred long before construction begins.

Land acquisition, zoning approvals, environmental reviews, infrastructure installation and permitting requirements all add layers of cost, time and risk. According to NAHB, regulatory costs alone account for nearly one-quarter of the final price of a new single-family home.

Rising land prices reflect a combination of limited supply, competition from institutional investors, and the high cost of extending infrastructure such as roads, water, sewer and utilities. In many markets, regulatory complexity and lengthy approval timelines further constrain the availability of buildable lots, pushing builders toward higher-priced homes that can absorb these upfront costs and away from entry-level housing.

Compounding these challenges is a worsening labor shortage. Skilled trades—including carpenters, electricians, plumbers and masons—are in critically short supply. The National Center for Construction Education and Research (NCCER) estimates that more than 40 percent of the current construction workforce is expected to retire by 2031. This impending loss of experience and institutional knowledge threatens to further slow production and increase costs unless workforce development pipelines are expanded.

Implications for the Concrete Industry

The pressures shaping today’s housing market extend beyond homebuilders and directly influence the concrete industry, which sits at the front end of nearly every construction project. From site development and infrastructure to foundations and flatwork, concrete contractors and suppliers experience market shifts early in the construction cycle. As production slows or accelerates, the effects are felt immediately in demand, scheduling, labor needs and investment decisions across the sector.

Demand Volatility and Production Planning

Elevated interest rates and affordability constraints have moderated housing starts in many markets, creating uneven production cycles for builders. Because concrete work typically begins shortly after site development, fluctuations in starts translate directly into inconsistent demand for foundations, slabs and infrastructure work. Contractors face periods of intense scheduling pressure followed by slowdowns that make workforce retention and equipment utilization more difficult to manage. While long-term housing demand remains strong, short-term production variability complicates forecasting and operational stability for concrete producers.

Development Delays Reduce Early-Stage Construction Activity

Challenges associated with land development—ranging from regulatory approvals to infrastructure costs—also impact the concrete industry at the earliest stages of construction. Roads, utilities, sidewalks and community infrastructure all rely heavily on concrete, meaning delays in permitting or development approvals slow the flow of projects entering construction. As builders phase projects more cautiously, concrete contractors often encounter gaps between community launches and reduced lot availability, further contributing to uneven production schedules.

Labor Shortages Intensify Operation Pressure

Like many construction trades, the concrete industry faces an aging workforce and limited replacement labor entering the field. The physically demanding nature of concrete work, combined with competition from other industries for skilled workers, has made recruitment and retention increasingly difficult. Labor constraints can extend project timelines, increase wage pressure and limit the number of crews available to support expanding housing demand. Without sustained workforce development efforts, labor availability will remain a constraint on production capacity.

Shift Toward Higher-End Construction Changes Project Mix

Rising development and regulatory costs have pushed many builders to focus on higher-priced homes that can better absorb upfront expenses. For concrete contractors, this shift often results in fewer entry-level housing projects and greater involvement in custom or move-up construction. While these homes may require more complex foundations and specialized work, overall unit volumes may decline compared to entry-level production, altering workload consistency and planning assumptions.

Margin Pressure Throughout the Construction Supply Chain

Affordability challenges continue to place pressure on builders seeking ways to control total construction costs. As competition increases and incentives become more common, cost scrutiny extends throughout the supply chain, including concrete services. Contractors must balance maintaining quality and safety standards with the need to operate efficiently in a market where price sensitivity is increasing among both builders and buyers.

Affordability Is the Wild Card

While home price growth has moderated in parts of the country, affordability remains the defining issue for the U.S. housing market. Higher mortgage rates, elevated construction costs and tighter lending conditions have significantly reduced purchasing power for many households. According to the National Association of Realtors, the share of median-income households able to afford a median-priced new home has fallen sharply compared to pre-pandemic levels.

Builder margins, which increased during the post-pandemic period due to pricing power and constrained supply, may face pressure going forward as land and development costs continue to rise and incentives become more common. However, margins remain elevated relative to historical norms, reflecting disciplined production strategies and a market that continues to favor sellers over buyers.

National affordability data show a clear mismatch between household incomes and the price points of newly built homes. Demand remains strongest in the entry-level and moderate-price segments, yet much of today’s new construction is concentrated at higher price points. This disconnect places increasing strain on first-time and middle-income buyers and underscores the need for policy and regulatory reforms that enable the production of attainable housing.

Policy Levers that Can Make a Difference

Addressing the national affordability challenge will require coordinated action across all levels of government. Potential solutions include:

- Incentivizing responsible development through tax abatements, expedited permitting or fee reductions for projects that include attainable housing.

- Modernizing zoning and land-use regulations to allow greater density, smaller lot sizes and more efficient use of existing infrastructure.

- Expanding infrastructure investment through state and federal funding partnerships that support housing production.

- Strengthening workforce development by investing in trade education, apprenticeships and career pathways in the skilled trades.

- Encouraging adaptive reuse and redevelopment of underutilized commercial and industrial properties.

- Improving predictability in the development process by standardizing review timelines, fees and regulatory requirements.

- Supporting buyers through targeted down payment assistance, tax incentives and mortgage affordability programs.

If policymakers can reduce uncertainty and share the burden of high upfront development costs, builders will be better positioned to deliver homes at price points that align with what American households can realistically afford.

The Future Will Be Built by Deliberate Action

The challenges facing the U.S. homebuilding industry—persistent inflation, labor shortages, regulatory complexity and supply constraints—are unlikely to resolve quickly. While national trends suggest that supply and demand imbalances may gradually improve, the concrete industry remains central to addressing the nation’s housing shortage. Every effort to increase housing production—whether through expanded development, infrastructure investment or more efficient construction methods—requires concrete at scale. As the housing market works toward restoring balance between supply and demand, the capacity, efficiency and workforce strength of the concrete industry will play a critical role in determining how quickly new housing can be delivered.