Professional Liability: Are Contractors Adequately Protected?

Español | Translation Provided by the CFA

As the lines of responsibility between design firms and contractors merge, contractors are assuming nontraditional risk that their core insurance coverages may not address. Professional liability coverage has become just as essential to a contractor as it is to an architect or engineer. Learn about the contractor’s professional exposure, potential damages, and alternative solutions and insurance options in this insightful article.

Fred Muse

Design and Professional Liability

In traditional project delivery (design-bid-build), an architect or engineer provides design services while actual construction or implementation of the design is carried out by the contractor. Under this scenario, you may expect that the potential liabilities facing the design professional and contractor would be fairly well defined. However, as the complexity of projects increases and new construction contracts are introduced, design responsibilities are becoming more fragmented. In addition, project owners are requiring their contractors to take on additional construction management activities and, with greater frequency, are looking for the contractor to provide a single point of responsibility for design and construction.

As the lines of responsibility between design firms and contractors merge, contractors are assuming nontraditional risk that their core coverages may not address. In this article, we are going to review activities that increase a contractor’s professional risk and then discuss how well the liability insurance is responding. You may discover that professional liability coverage will become just as essential to a contractor as it is to an architect or engineer.

Understanding Contractor’s Professional Risk Exposure

New methods of project delivery have created challenges and exposures that need to be understood, assessed, and adequately insured by the parties accepting the risk. One of the most significant challenges faced by the project participants and their risk managers is identifying and managing the risks when the design and engineering responsibilities are shared and fragmented among many project participants.

Contractors Professional Liability Chart

Today, when a primary architect is hired to design the entire project, other parties outside the architect’s control will be involved with the design. Contractor responsibilities are often expanded beyond construction to include professional risk associated with construction management, design delegation, hiring design firms, and actually self-performing design. These are discussed in more detail below.

Construction Management Responsibilities: A contractor may perform construction management services as the owner’s agent (agency construction management) or they may also hold separate contracts with the trade subcontractors (at-risk construction management). In both situations, the contractor takes on responsibility for supervision of the subcontractors, scheduling, and cost estimating. All these activities create a recognized standard of care by the construction manager and a corresponding professional liability risk.

Design Delegation: Based on “performance” specifications, specialty subcontractors have effectively designed curtain wall and sprinkler systems for years. In addition, the contractor’s mechanical and electrical subcontractors are often engineering the heating, ventilating, and air conditioning (HVAC) and other systems. Currently, the 1997 version of the AIA A-201 General Conditions Document specifically outlines when design may be delegated to the contractor with a corresponding waiver of liability by the architectural team.

Hiring Design Firms as Subcontractors or A/E Joint Venture: A growing number of projects are utilizing design-build project delivery where the contractor is acting as the lead design-builder or enters into a joint venture with a design firm. When a contractor assumes a single point of responsibility role for an owner by use of the design-build project delivery, they are now responsible for project design in addition to their construction obligations. In addition to design-build project delivery, the project owner may hire separate design consultants to provide the interior design, landscape architectural, or other services and then assign these contracts to the contractor.

Self-Performed Design: Some contractors have an in-house design staff consisting of legally qualified architects, engineers, land surveyors, and landscape architects who have the responsibility for reviewing and stamping drawings.

Potential Contractor Damages Resulting from Professional Liability Risk

Errors and omissions associated with performing professional services can result in costly time delays, budget overruns, rework, and third-party bodily injury and/or property damage. Knowing and anticipating this financial risk can make the difference between a profitable project and one that ends up in costly litigation for years.

Economic Loss: There are significant financial risks that contractors assume by promising to deliver a project complete, on time, and within budget. Claim examples include the following.

- Design Delegation — The contractor subcontracts the design of a ventilation system to a mechanical engineer. The engineer, who did not carry errors and omissions (E&O) insurance, miscalculated the cooling needs of the building and specified an inadequate ventilation system. The building owner demanded $180,000 to replace the poorly performing system.

- Design Error — The contractor made a cost estimate of $2 million for a warehouse project. A loading platform was later found to be inadequate to meet the stated needs of the warehouse. With the revisions, the project cost $2.5 million. The contractor was held liable for the $500,000 difference.

Third-Party Bodily Injury or Property Damage: Design errors have contributed to some of the most catastrophic losses resulting in direct damage to the project and fatalities to both construction workers and members of the public. These types of claims have occurred both during construction and after the project has been turned over to the owner. Claim examples include the following.

- Design Delegation — In a “sick building syndrome” claim, a subcontractor improperly designed and installed an HVAC system. Mold formed in the chillers, and the air in the building made people ill. Multiple claimants filed suit against the contractor in addition to the owner who suffered business interruption losses.

- Construction Management — A contractor failed to detect the faulty workmanship of a masonry contractor who placed hollow concrete block without proper re-bar reinforcement as specified in the plans. Once discovered, the structure had to be torn down and rebuilt at a cost of approximately $1 million plus resulting delays in project completion.

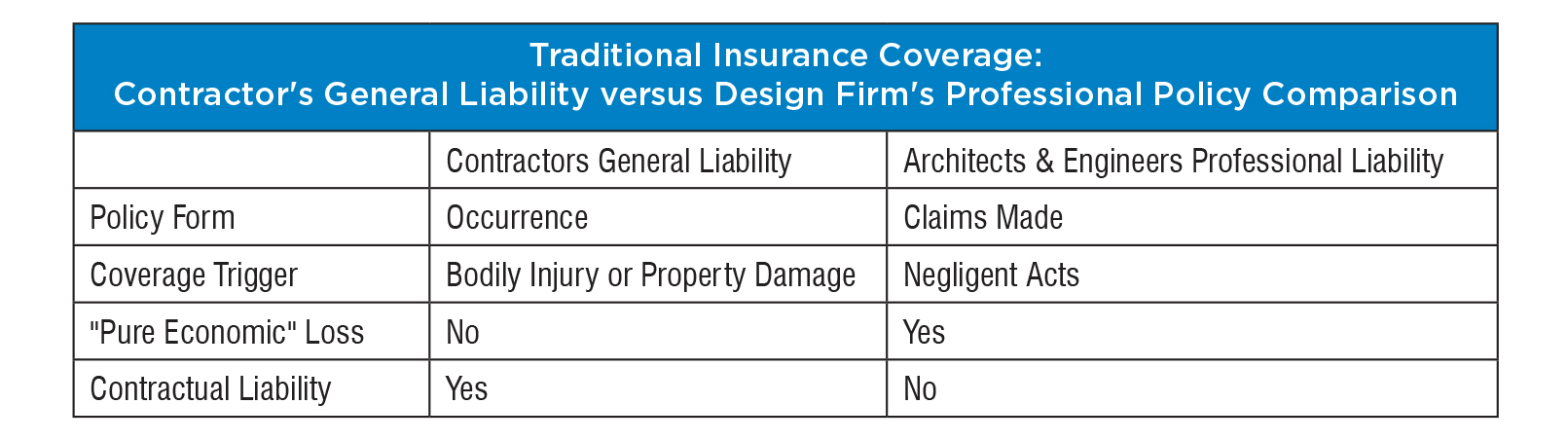

Before we examine the availability of traditional coverages for professional risk, it is critical to first understand the fundamental differences between a general liability and professional liability policy. Basically, general liability policies will cover losses caused by “ordinary construction means and methods” as long as it results in bodily injury and/or property damage arising from an occurrence. Professional liability policies cover any damages that arise from the rendering or failure to render professional services.

For example, under the general liability policy, project delays and cost of reinforcing a faulty structure would not be covered unless there was a corresponding occurrence that resulted in bodily injury or property damage. However, this type of claim would be covered under a professional liability policy as long as it was caused by professional negligence. It is important to note that negligence occurs when services are not performed with the standard of care exercised by any other design professional facing the same or similar facts and circumstances.

Contractor’s General Liability Policy: A general liability policy without a professional exclusion amendment can provide limited protection for design errors as long as the loss results in bodily injury or property damage. However, many insurers will attach an endorsement to their contractor’s policies that excludes liability arising from design error (Insurance Services Office, Inc. (ISO), Form CG 22 43). At a minimum, this exclusion needs to be clarified so that excluded professional services will not incorporate any activities included within construction means or methods (ISO CG 22 79).

Another endorsement, “Limited Exclusion — Contractor Professional Liability Endorsement,” gives back coverage for bodily injury or property damage from professional design services in connection with a project the contractor is also constructing (ISO CG 22 80). Even if the contractor is successful in amending the primary policy, this does not guarantee that the lead umbrella or excess limits will follow form.

Design Firms Professional Liability Policy: When a contractor leads a design-build project and hires an architect/engineer as a subcontractor, the contractor may rely on the professional liability policy of the design firm. However, it is important to know the limitations associated with the architect or engineer’s annual practice professional coverage.

- Single Aggregate Limit — The policy limit applies to all current and past work and the limit includes defense cost. If you have a claim, you could be sharing the limit with many other firms.

- Low Limits — A majority of design firms carry professional limits of $1 million or less.

- Claims-Made Policy — If the design firm nonrenews their policy or moves the retroactive date forward after they finish your project, you will be left with no protection.

- No Additional Insured Protection — Most professional liability underwriters for design firms will not name another firm as an additional insured.

Traditional Professional Cover

Alternative Solutions for Contractors Professional Coverage

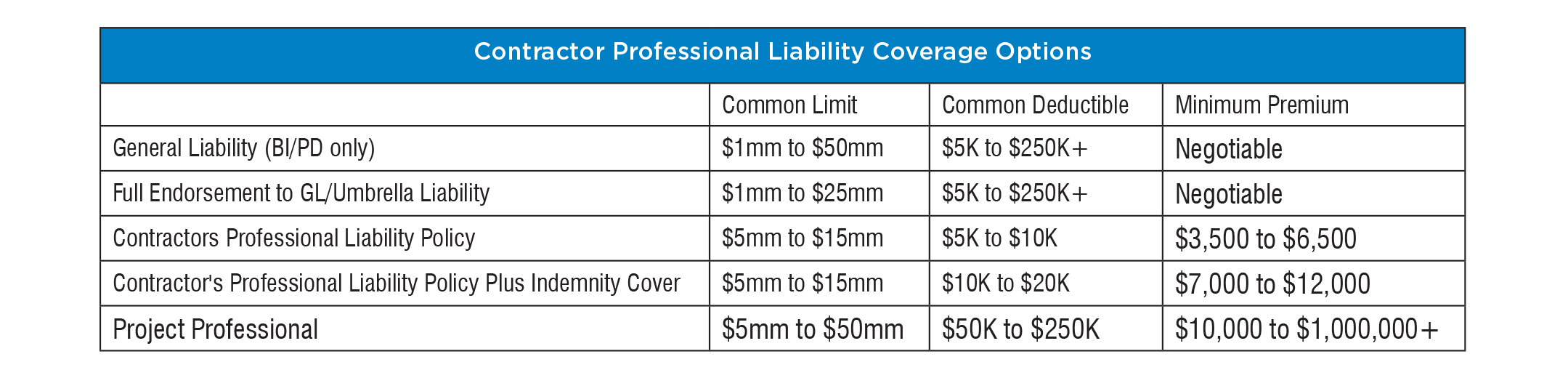

Additional coverage is now available for contractor’s professional risk that traditionally may have been considered business risks that are not insurable. Full professional liability insurance for a contractor can be purchased as an add-on to a general or umbrella liability policy, covered under a stand-alone contractor’s professional policy, or handled under a separate project professional policy.

Endorsement to General or Umbrella Policy: True professional coverage can be added on an “occurrence” basis to an existing general liability policy. This option does offer the advantage of providing high limits at a relatively low cost. However, this coverage is normally more restrictive than a “stand-alone” policy and is not offered to contractors who have in-house design capabilities. In addition, there are only a few underwriters who provide this option, and none offer both primary and umbrella coverage.

Contractors Professional Liability Policy: This coverage is written on a “claims-made” basis and insures a contractor for damages arising out of negligence of the contractor or its subconsultant architect/engineer in performing professional services under the contract. The policy includes coverage for a wide array of professional circumstances including design errors from a contractor’s:

- In-house design staff

- Design delegation under provisions of AIA A-201 General Conditions Document

- Subcontracting design under a design-build contract

- Agency and at-risk construction management

- Faulty workmanship of subcontractors when there is a construction management contract

- Pollution Coverage — In addition, most insurers providing this coverage will add “Contractors Pollution” coverage to the policy that will cover pollution claims arising from job-site activities and failure to detect or quantify the presence of pollutants.

- Indemnity Coverage — For an additional premium, there is one insurer that will provide coverage for first-party claims by a contractor against its architect/engineer. To recover under the policy, the contractor must demonstrate that the design professional is legally liable to the contractor for the loss. Although the policy is designed to be excess of the architect/engineer’s underlying insurance, coverage will drop down to a lower self-insured retention (SIR) in the event that the architect/engineer’s policy has been eroded by other claims. In addition, if this policy is broader than the underlying design firm policy, indemnity coverage will provide the contractor with difference-in-conditions coverage.

Project Specific Professional Coverage: For larger or more complex projects, the owner may elect to purchase a separate policy that will provide a single source of recovery for all professional liability losses related to their project (see IRMI.com, Project-Specific Professional Liability: Who Really Pays for Design Errors?). The policy replaces the annual professional liability coverage provided by individual design firms, construction manager, general contractor, and subcontractors. While this approach can provide significant, noncancelable limits that can be in place up to 10 years after the project is completed, the contractor should review the following policy terms and conditions carefully.

- “Who is an insured” — The contractor and subconsultants should be named.

- “Insured versus insured exclusion” — This should be deleted.

- Policy deductible — A sharing agreement should be drafted.

Conclusion

Even with the most basic forms of project delivery, there is an increased chance of having fragmented design responsibility. Before a project is started, all participants should be satisfied that professional risks have been adequately assessed and insured by the responsible parties. The contractor needs to have assurance that professional coverage will be in place when a design error is discovered, especially after project completion, and that the limits are adequate. The addition of a contractors professional policy can provide broad protection for alleged errors or omissions in the delivery of design and construction management services.

Opinions expressed in Expert Commentary articles are those of the author and are not necessarily held by the author’s employer or IRMI. Expert Commentary articles and other IRMI Online content do not purport to provide legal, accounting, or other professional advice or opinion. If such advice is needed, consult with your attorney, accountant, or other qualified adviser.